How I Tackled My Debt Without Losing Sleep – Real Product Picks That Worked

Dealing with debt felt overwhelming at first—like running on a treadmill going nowhere. I tried quick fixes that made things worse. But slowly, I found tools and products that actually helped me regain control. This isn’t about get-rich-quick schemes; it’s about practical choices that align with real life. If you’re starting your debt repayment journey, you’re not alone—and the right product selection can make all the difference. What began as a cycle of stress and avoidance turned into a structured, manageable path forward. Along the way, I learned that financial recovery isn’t just about numbers—it’s about making thoughtful, sustainable decisions. The tools you choose matter more than most people realize, and the wrong ones can cost you time, money, and peace of mind.

The Moment Everything Changed: Facing Debt Head-On

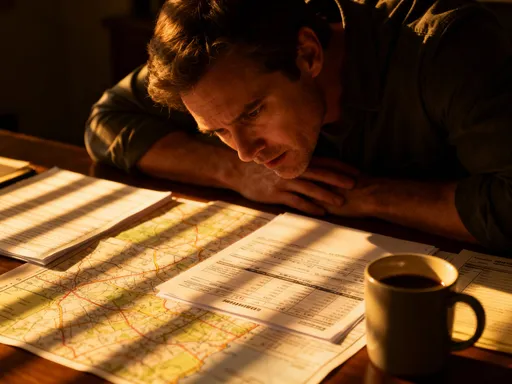

For months, I avoided opening my mailbox. Bills piled up in a drawer I refused to touch. Each envelope represented not just money owed, but a failure I wasn’t ready to face. I told myself I’d deal with it “next month” or “after the holidays,” but deep down, I knew I was delaying the inevitable. The turning point came on a quiet Sunday morning when I finally sat at my kitchen table with a cup of tea and every statement I’d ignored. As I spread them out, the total amount stunned me. It wasn’t just the number—it was the weight of what it represented: years of small, unexamined choices that had quietly snowballed into something unmanageable.

That moment could have paralyzed me, but instead, it sparked clarity. I realized I wasn’t alone—millions of people carry debt, and many of them feel the same mix of shame and fear. What changed was my mindset: I stopped seeing debt as a moral failure and started seeing it as a financial challenge with practical solutions. This shift didn’t erase the numbers, but it created space for action. I began researching repayment strategies, not with desperation, but with purpose. I understood that before I could fix the problem, I had to stop hiding from it. Acknowledging the full scope of my obligations was the first real step toward regaining control.

From that day forward, I committed to transparency—with myself, and eventually, with my family. I created a simple spreadsheet listing every debt: the creditor, balance, interest rate, and minimum payment. Seeing it all in one place was uncomfortable, but also empowering. It turned an abstract fear into a concrete plan. I didn’t need a miracle; I needed a method. And part of that method would be choosing financial products that supported my goals, rather than ones that offered false promises or complicated my situation further. The emotional burden began to lift as I focused on progress, not perfection.

Why Product Choice Matters More Than You Think

Once I had a clear picture of my debt, I started looking for tools to help me pay it off faster. My first attempt was a balance transfer offer I saw advertised online—a 0% introductory rate for 18 months. It sounded perfect: move high-interest credit card balances to one card, pay no interest, and knock out the debt within the promotional period. I signed up quickly, eager for relief. But within months, I realized I’d made a costly mistake. The transfer fee was higher than I’d calculated, and because the new card had a lower credit limit, I couldn’t move all my debt. Worse, I missed a payment during a busy week and lost the promotional rate entirely. Instead of saving money, I was now paying even more in interest.

This experience taught me a crucial lesson: not all financial products are designed with the user’s long-term success in mind. Some prioritize short-term gains or hidden revenue streams over genuine debt relief. The right products, however, can be powerful allies. A low-fee balance transfer card with a realistic timeline, for example, can save hundreds in interest if used carefully. Similarly, structured repayment apps that sync with bank accounts and send gentle reminders can keep users on track without adding stress. Credit-builder accounts, often overlooked, offer a way to improve credit scores while saving small amounts regularly—essential for those rebuilding financial stability.

What makes a product truly helpful isn’t just its features, but how well it aligns with real-life financial behavior. Automation, transparency, and ease of use are often more important than flashy promises. A tool that requires constant manual input or has confusing terms will likely be abandoned. On the other hand, one that integrates smoothly into daily routines—like automatically allocating extra funds toward debt when a paycheck comes in—can create momentum. The key is understanding that product choice isn’t just about cost or convenience; it’s about sustainability. The best tools support consistent progress, even during busy or stressful times.

Moreover, the cumulative effect of small advantages can be significant. A product that saves $10 a month in fees may not seem like much, but over five years, that’s $600—money that could go toward principal reduction or an emergency fund. Similarly, avoiding a single late fee or interest rate hike can prevent a spiral that sets repayment back months. This is why careful evaluation matters. It’s not enough to choose something because it’s popular or easy to sign up for. The right product should fit your specific situation, reduce friction, and help you stay focused on your goal.

Sorting the Helpful from the Hype: My Testing Process

Determined not to repeat my earlier mistakes, I decided to test multiple debt management tools before committing to any one solution. Over six months, I tried six different products—some free, some with monthly fees—ranging from budgeting apps to specialized debt payoff platforms. My goal wasn’t to find the most feature-rich option, but the one that worked best in real life. I evaluated each based on four key criteria: ease of setup, transparency of terms, quality of customer support, and actual impact on my monthly habits.

The first app I tried promised to “automate your debt freedom” with AI-driven payment plans. Setup was smooth, but within two weeks, I received an email pushing a premium subscription with a 30-day trial that required a credit card. I almost missed the cancellation deadline, and the process was frustratingly opaque. That was my first red flag: automatic upsells. A trustworthy product should be clear about costs from the start and never trap users in subscriptions they didn’t intend to keep. I also noticed that the app didn’t sync accurately with one of my bank accounts, leading to incorrect balance displays. For someone trying to track progress precisely, that kind of error could lead to overspending or missed payments.

Another tool I tested offered a debt consolidation loan with a slightly lower interest rate than my current cards. On paper, it looked beneficial. But when I read the fine print, I discovered a prepayment penalty—if I paid off the loan early, I’d owe an additional fee. That defeated the purpose of wanting to accelerate repayment. I walked away, realizing that even seemingly straightforward products can have hidden trade-offs. What I appreciated most in the tools that worked was clarity: no confusing jargon, no surprise charges, and a clear path to cancel or switch services if needed.

I also relied heavily on trial periods and small initial commitments. Instead of transferring all my debt at once, I moved a small balance to test how a new card or platform handled payments and reporting. This approach protected me from large-scale mistakes. One app, for example, offered a free version with core features and only prompted for upgrades when I accessed advanced tools—on my terms. It respected my autonomy and provided real value without pressure. By the end of my testing phase, I had a shortlist of two tools that consistently supported my progress: a simple auto-pay system linked to my primary credit card and a budgeting app with reliable syncing and clear visual progress tracking.

The Role of Automation in Staying on Track

Before I embraced automation, my repayment efforts were inconsistent. I’d make payments on time for a few months, then miss one during a hectic week. Each late payment came with a fee and a spike in stress. I blamed myself—surely, I should be disciplined enough to remember. But life is unpredictable: children get sick, work deadlines pile up, and even the most organized person can drop the ball. That’s when I realized I didn’t need more willpower; I needed a better system. Automation became my turning point.

I started by setting up auto-pay for the minimum amount on all my credit cards. It wasn’t enough to eliminate debt quickly, but it prevented late fees and protected my credit score. Then, I added a second layer: a separate savings account where I programmed small, automatic transfers each payday. This “debt payoff fund” grew steadily, and every month, I manually transferred a lump sum to my highest-interest card. Over time, I refined the process—increasing the auto-transfer amount as my budget allowed and using round-up features on debit card purchases to add extra dollars without noticing the loss.

What surprised me most was how much mental energy this saved. I no longer had to debate whether I could afford an extra $50 this month or remember due dates. The system handled it. This shift from constant decision-making to consistent action created momentum. Even when I felt discouraged, the payments kept going. Automation turned repayment from an emotional burden into a quiet, reliable habit. It didn’t require motivation—just setup.

Another benefit was the reduction in temptation. When extra money sat in my checking account, it was easy to justify spending it on something “urgent” or “deserved.” But when it automatically moved to a separate account, it felt less accessible—and more purposeful. I began to see that account not as lost money, but as progress in motion. Tools with visual trackers, like progress bars or payoff calendars, reinforced this feeling. Watching the balance shrink month after month, even slowly, built confidence. Automation didn’t solve everything, but it removed the biggest obstacles: forgetfulness, inconsistency, and emotional decision-making.

Balancing Risk and Reward in Debt Tools

As I narrowed down my options, I became more aware of trade-offs. Some products promised fast results but carried long-term costs. A debt settlement company, for example, offered to negotiate my balances down by 40%. It sounded appealing—until I learned it could severely damage my credit score and that success wasn’t guaranteed. Even if it worked, the negative mark could stay on my report for years, affecting future loans or rental applications. I decided the risk outweighed the potential reward.

Similarly, I considered a personal loan with a low introductory rate, but the terms included a variable interest rate after the first year. If rates rose, my payments could become unaffordable. I also looked into credit counseling services, which can be helpful, but discovered that some agencies charge high setup fees or require long-term enrollment. Without careful vetting, I could trade one financial burden for another. This taught me to approach every option with balanced skepticism: not dismissive, but cautious.

I developed a simple risk-assessment checklist. First, I asked: Does this product require me to take on new debt? If yes, is the interest rate lower and the repayment term manageable? Second, what are the credit implications? Will it trigger a hard inquiry or lower my average account age? Third, are there penalties for early payoff or missed payments? Fourth, how transparent is the provider about fees and terms? If the answers raised concerns, I kept looking.

This process helped me avoid tools that prioritized their profit over my progress. Instead, I focused on solutions with fixed rates, clear exit strategies, and no hidden penalties. Risk awareness didn’t make me risk-averse—it made me strategic. I learned that sustainable debt repayment isn’t about eliminating all risk, but about making informed choices. The goal wasn’t to find a perfect solution, but one that aligned with my tolerance for uncertainty and my long-term stability.

Matching Products to Personal Financial Behavior

One of the biggest surprises in my journey was realizing that a tool that worked wonders for a friend nearly derailed my progress. She swore by a strict zero-based budgeting app that allocated every dollar in advance. For her, it brought clarity and control. For me, it felt suffocating. I have irregular income due to freelance work, and trying to assign every cent left me anxious and discouraged when reality didn’t match the plan. I quickly abandoned it, not because the tool was bad, but because it didn’t fit my financial behavior.

This experience led me to reflect on my own patterns. I’m more responsive to flexibility than rigidity. I do better with systems that adapt to life’s changes rather than demand constant adjustments. I also respond well to simplicity—too many features or complex dashboards overwhelm me. With this self-awareness, I began selecting products that matched my reality. I chose a budgeting app with a “set it and forget it” approach, where income and expenses update automatically, and I only intervene when needed.

I also considered my emotional triggers. I’m prone to stress spending during busy seasons, so I built in safeguards: a separate account for discretionary spending with a monthly cap, and a rule that any purchase over $50 required a 24-hour waiting period. The tools I used supported these rules—some even sent alerts when I approached my limit. This wasn’t about restriction; it was about creating a framework that anticipated my weaknesses and turned them into manageable habits.

Matching products to behavior also meant accepting that I wouldn’t always be perfectly consistent. Life happens. So I prioritized tools with grace periods, no-penalty adjustments, and responsive customer service. The goal wasn’t to build a flawless system, but a resilient one—one that could bend without breaking. Self-awareness became the foundation of my success. By choosing tools that worked with my nature, not against it, I built a repayment strategy that felt sustainable, not stressful.

Building a Sustainable System, Not Just a Quick Fix

Looking back, I realize that my debt repayment wasn’t the result of a single tool or a dramatic lifestyle change. It was the outcome of building a system—a quiet, consistent approach that combined the right products, the right account structure, and the right habits. I linked auto-pay to my primary debt, used a separate savings account for extra payments, and relied on a simple budgeting app to monitor progress. None of these were revolutionary on their own, but together, they created a rhythm that carried me forward.

The most important shift was moving from intensity to consistency. Early on, I tried to pay huge amounts, cutting out all extras to accelerate progress. But that approach was unsustainable. When I inevitably slipped—buying medicine for a sick child or fixing a car—I felt like a failure and sometimes gave up altogether. Over time, I learned that small, reliable actions are more powerful than occasional bursts of effort. Paying an extra $25 every month, without fail, builds more momentum than paying $200 once and then stopping.

This system also protected my peace of mind. I no longer lay awake worrying about missed payments or surprise fees. The automation handled the details, and the transparency of my tools kept me informed. I could see my progress, celebrate small wins, and adjust as needed—without panic. Debt repayment became less about sacrifice and more about stewardship. I wasn’t just paying off the past; I was building a more secure future.

Today, I’m not debt-free, but I’m on track—and more importantly, I’m in control. The tools I use continue to support me, and I’ve added a small emergency fund to prevent future setbacks. My journey taught me that financial healing isn’t about perfection. It’s about progress, protected by thoughtful choices and sustainable systems. If you’re facing debt, know that you don’t need a miracle. You need a plan, the right tools, and the courage to start. And sometimes, the quietest steps lead to the most lasting change.